Savills report notes strong third-quarter performance, with Districts 2 and 9 dominating.

Ho Chi Minh City’s villa/townhouse segment recorded robust performance in the third quarter of the year, according to the latest report from Savills on the city’s real estate market, released on October 11.

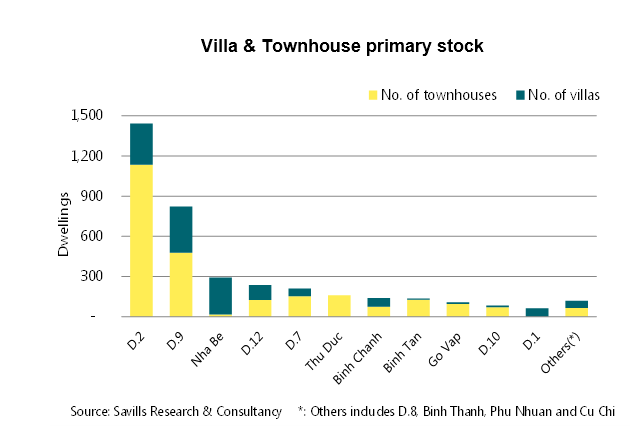

Six new projects and subsequent phases of five existing projects provided approximately 1,100 dwellings to the primary market. Primary stock reached approximately 3,800 dwellings, up 19 per cent quarter-on-quarter and 128 per cent year-on-year.

Sales increased 49 per cent quarter-on-quarter and 193 per cent year-on-year due to good performance in the new projects. Townhouses dominated with 71 per cent of total transactions. Absorption was 32 per cent, up 7 ppts quarter-on-quarter and 8 ppts year-on-year.

Districts 2 and 9 continued to outperform other districts, cumulatively accounting for 51 per cent of sales.

“Well-developed infrastructure and urban planning supported strong sales in the east of Ho Chi Minh City,” the report stated. “Projects with credible developers, appropriate pricing and a wide range of facilities remained key criteria of buyers.”

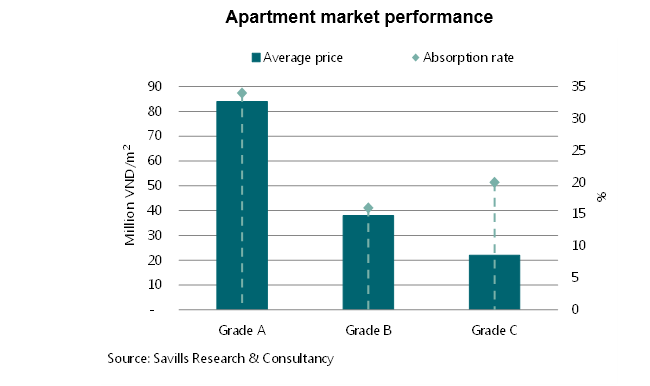

Regarding apartments, the report showed that sales in Grade C increased sharply. Eleven new projects and the next phase of one active project launched, supplying more than 4,600 units, representing a significant decrease of 47 per cent quarter-on-quarter. There were approximately 40,300 available units across all grades.

Sales reached 7,500 units, increasing 7 per cent quarter-on-quarter and 43 per cent year-on-year. Absorption was 19 per cent, increasing 2 ppts quarter-on-quarter and year-on-year due to good Grade A and C performances.

Grade A had the highest absorption at 34 per cent. Grade C transactions increased dramatically by 15 per cent quarter-on-quarter. Grade B sales fell 12 per cent quarter-on-quarter after six consecutive quarters of increases.

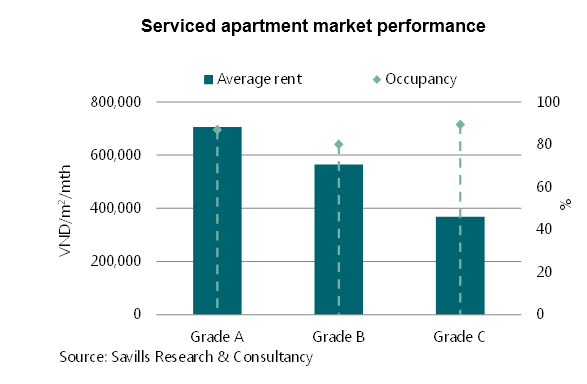

The serviced apartment segment, meanwhile, saw a slight increase in supply. Total serviced apartment stock was approximately 4,540 units from 83 projects, relatively stable quarter-on-quarter due to the re-entry of one Grade C project in Phu Nhuan district with five units and up 4 per cent year-on-year.

All grades showed marginal quarterly performance improvements. Average occupancy was up 3 ppts quarter-on-quarter and 2 ppts year-on-year to 84 per cent, with Grades A and B enjoying the strongest occupancy increases.

Average rents have improved since the first quarter, marking a recovery from three consecutive years of downward adjustments. Average rent was VND529,000 ($24) per sq m per month, relatively stable quarter-on-quarter but up 2 per cent year-on-year.

Competition from a large future supply of high-end buy-to-let apartments will create pricing pressure. From the fourth quarter to 2018, 12 serviced apartment projects providing 2,150 units are expected to enter the market.

The CBD will remain the investment hotspot, accounting for 64 per cent of total future supply to the end of 2018.